Unless you have been living under a rock, you are probably aware of the ongoing government shutdown. If you are a non-government worker, you may think that this will have little impact on you, but the effects may be more far reaching than you think. The shutdown includes all non-essential government employees and the many departments they represent. Some of these departments are directly related to the mortgage process. If you are selling a home, your buyer could directly be affected. Furthermore, if you are buying, the process may be stalled until there is some resolution. Regardless, the government shutdown will have a negative impact on the real estate market.

Even if you aren’t applying for a government loan, your application could directly be impacted. Most lenders need verification of income and identity through the Internal Revenue Service (IRS) or the Social Security Administration to process the loan. Even though income fraud and identity theft for the purposes of a mortgage application is very rare, it does happen. Lenders that underwrite these loans would be on the hook for the entire loan amount and unable to sell in the secondary market. Because of the shutdown, many lenders are forced to decide if the risk is worth the reward in lending without these important documents. Some lenders are forging on, but at the first sign of fraud, they will no doubt stop lending all together.

The longer the shutdown continues, the more likely something will come up and cause servicers to stop lending. This will have a trickle-down effect on rate locks, approvals and ultimately closings. A buyer that may have liked the property and the price may not feel the same way in 60 or 90 days. A seller that may have needed to sell to move somewhere else may be in a holding pattern for an undetermined amount of time.

Markets can adjust for a short term shutdown, but the longer it goes on, the more unstable things get. This may cause mortgage interest rates to fluctuate or shoot up if this lingers past our debt ceiling date. This increase may deter buyers from buying or may increase debt to income ratios and loan approvals. If buyers aren’t buying, then demand is lowered and this would cause a drop in home values. It is uncertain if the economy could withstand another drop in values, considering how much it took to finally get to this point.

This is not even accounting for buyers or sellers who are directly applying for FHA or VA loans. Those are direct government loans that are underwritten by these departments. For now they are continuing approvals, but the staffs have shrunk to skeleton crews. These loans make up anywhere from 15-30% of all new home purchases. With a decreased staff, this will cause an increase in loan turnaround times. It may make sellers or buyers consider walking away from the deal instead of waiting for 60 days. That will push parties into the holidays or near the first of the year.

There is no doubt that the sooner this gets worked out, the better it would be for the mortgage and real estate market. There has been no direct impact yet, but with every passing day, there is the risk that the purchase market can stall. If that happens, the government will have its hands full with another mess.

Article published by & courtesy of: Than Merrill - https://www.thanmerrill.com/impact-government-shutdown-real-estate-market/

Compliments of:

Julius F Zatopek III – Broker/Owner

Zatopek Properties

Notices:

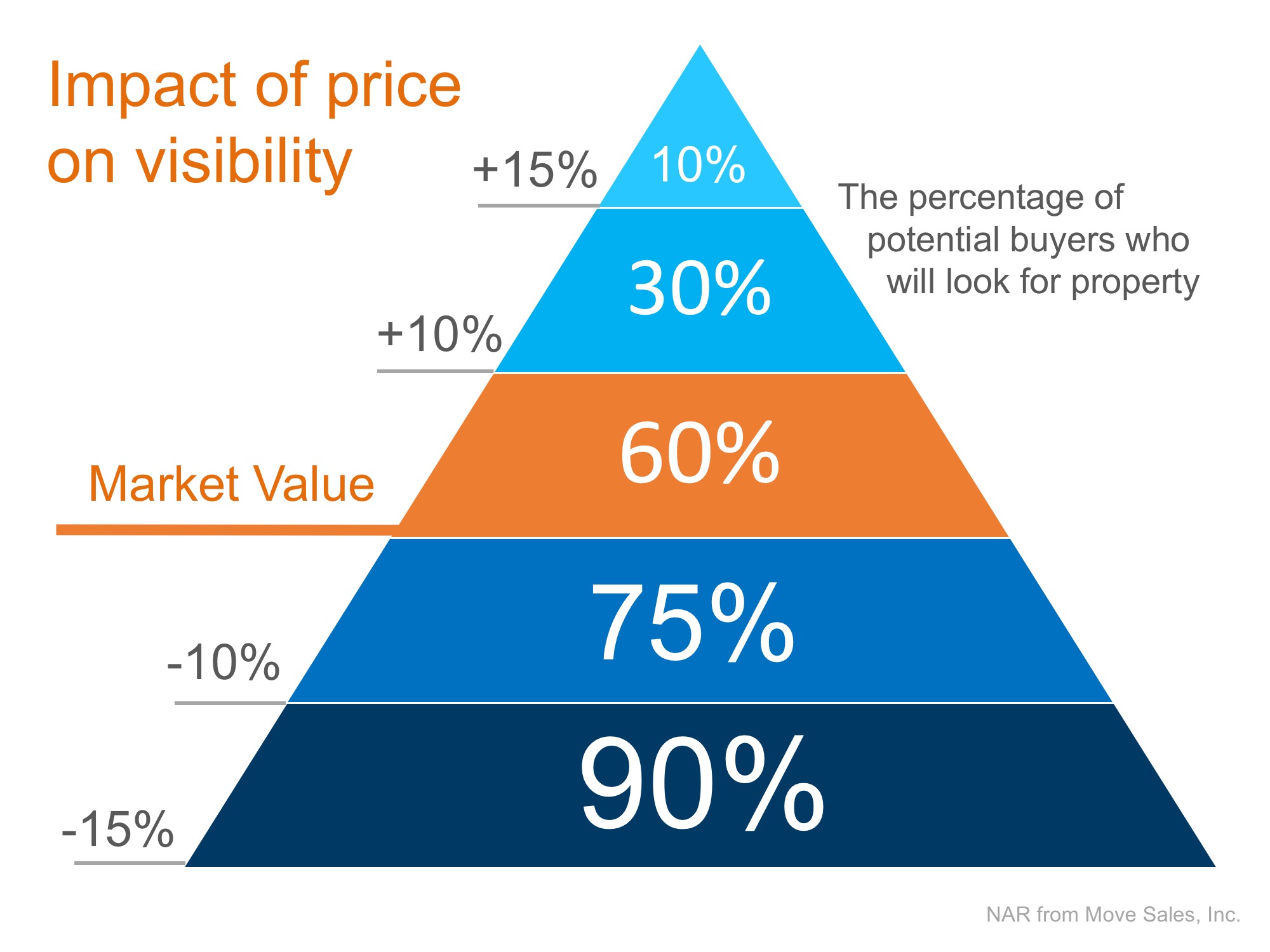

Every homeowner wants to make sure they maximize their financial reward when selling their home. But how do you guarantee that you receive the maximum value for your house?

Every homeowner wants to make sure they maximize their financial reward when selling their home. But how do you guarantee that you receive the maximum value for your house?